We'll be doing some work on our website on Tuesday 24 March which means you won't be able to log in, register, or apply online for a savings product between 6pm and 9pm.

Your annual mortgage statement is a helpful way to look back over the past year. It shows the payments you’ve made, how much interest you’ve been charged, any fees applied to your account and how much you still owe.

To make things easier, we’ve put together this simple guide – along with some FAQs – to walk you through your statement and explain what each section means.

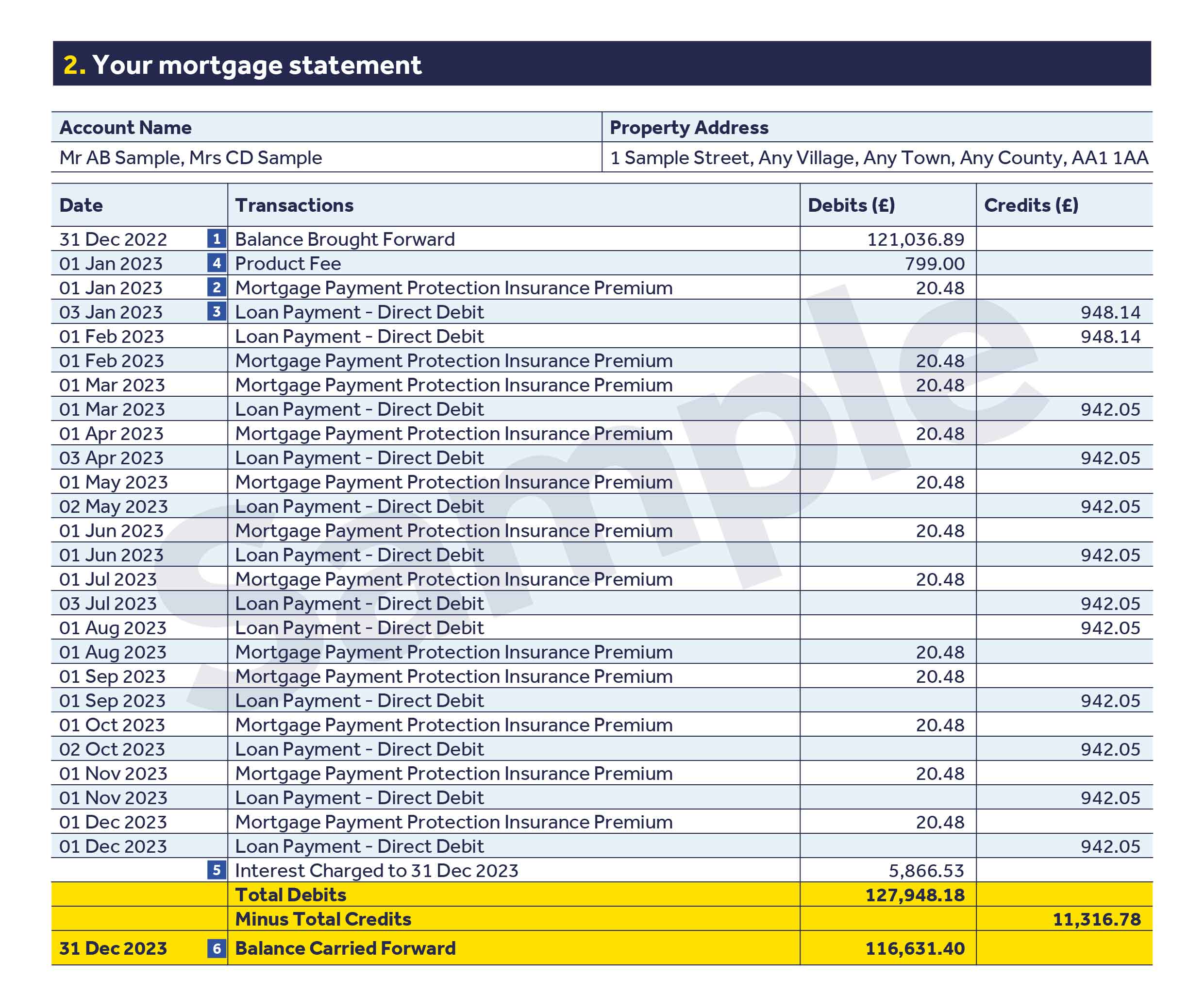

Here’s an example of a typical mortgage statement.

The blue numbers highlight the key areas, and you’ll find clear explanations for each one underneath the example.

1. Balance brought forward This is how much you still owed on your mortgage product(s) as of 31 December 2025. If your mortgage started after this date, we’ll show your start date and the full loan amount instead.

2. Loan payment All the payments you've made towards your mortgage will show in the 'Credits' column. Any refunds and returned or unpaid payments will appear in the 'Debits' column.

3. Fees Any fees or charges applied to your mortgage are shown in the 'Debits' column. Most entries include a short description, and you can find full details in our Tariff of Mortgage Charges. Sometimes you may make an extra payment to cover a fee, as shown in the example statement. If a fee or a charge is added without an additional payment, your mortgage balance will increase by that amount.

4. Interest charged This is the interest charged from 1 January to 31 December 2025, across all parts of your mortgage. The amount can change during the year if:

Your interest rate changes

You’ve made a lump sum capital payment

You take out additional borrowing

Interest is also charged on any fees or charges added to your mortgage.

5. Balance carried forward This is how much you still owed on your mortgage as of 31 December 2025, including all debits and credits shown on your statement.

6. Part number Your mortgage account might be split into different parts, which can have different interest rates, repayment types and terms. Each part will have its own number.

7. Product This is the product you’ve chosen for each part of your mortgage.

8. Repayment type This explains how each part of your mortgage will be repaid:

Capital and Interest -Your monthly payments go towards paying off some of the money you’ve borrowed (also known as capital), and some of the interest too. The amount you owe goes down with each repayment. If you make each monthly payment in full (and on time), you’ll pay off the mortgage by the end of the term.

Interest Only - You only make regular payments towards the interest on the mortgage and not the capital. You’ll owe the full balance of the money you borrowed when the mortgage ends.

Part and Part - Your mortgage is split between Repayment and Interest Only.

9. Balance This is how much you still need to pay on each part of your mortgage as of 1 January 2026.

10. Interest rate This is the interest rate for each part of your mortgage as of 1 January 2026.

11. Term end date This is when each part of your mortgage is due to end. It’s also when you’ll need to make a lump sum payment to repay any Interest Only balance(s) in full, if applicable.

12. Regulated part In the UK, the Financial Conduct Authority (FCA) regulates residential mortgages and certain buy to let mortgages taken out on or after 21 March 2016, where the property isn’t held for business purposes. If your mortgage falls within this category, you’ll benefit from certain protections under the regulatory system.

13. Interest rates applied in 2025 This is the interest rate applied to each part of your mortgage between 1 January and 31 December 2025, and the dates any changes took effect. These interest rates only apply to part(s) of your mortgage that were open last year, and don’t include details for any parts closed before 1 January 2026.

14. Monthly payments due These are all the payments that were due on your mortgage during 2025. You can compare these with the payments you made, shown in the 'Credits' column.

15. Amount to redeem your mortgage This figure shows how much it would cost to pay off your mortgage in full on 31 December 2025. It includes your remaining balance at this date, along with any possible repayment charges and exit fees.

Please note, this is just an illustration. No fees have been charged to your account, and they would only be charged if you choose to pay off your mortgage in the future.

This illustration was valid to 31 December 2025 and can’t be used for redemption purposes. If you’re thinking about paying off your mortgage, please get in touch with us for an up to date redemption statement.

16. Early Repayment Charges This is the Early Repayment Charge, if applicable under the terms of your mortgage product(s), calculated as of 31 December 2025 for each product.

We’ve created a handy online glossary of the most used mortgage terms to help explain things further. We hope it makes things easier, but if you have any questions or need extra support, please contact us.

Your mortgage statement questions

Your annual mortgage statement shows if the interest on your mortgage is worked out daily or annually.

If it’s annually, you can move to daily interest when changing to a new mortgage product (Early Repayment Charges may apply). You can’t switch from daily to annual interest.

Annual interest

Interest is worked out on your mortgage balance on 31 December each year. With annual interest, your monthly mortgage payments won’t reduce the balance on which interest is charged until that date.

Daily interest

Interest is worked out on your mortgage balance at the end of each day. The interest is charged to your account daily, increasing the mortgage balance by the amount of interest. Making your mortgage payments as early as possible in the month will reduce the balance and the amount of interest charged. However, this doesn’t apply to Interest Only mortgages.

This depends on the type of mortgage you have.

If any part of your mortgage has a variable interest rate, your monthly mortgage payment will go up or down whenever there’s a change to your interest rate. Whenever the rate changes, we’ll write to you and tell you about the new interest rate, your new monthly mortgage payment and when this will take effect.

If all your mortgage is fixed, your payments don’t normally change until your deal ends, unless you make any changes. These can include:

Making a large overpayment

Changing the term (length) of your mortgage

Changing how you repay your mortgage

Taking out additional borrowing

If your payment does change, we’ll let you know your new payment amount and the date the payment will change.

Your monthly payment could change for several reasons, such as:

Your mortgage is on a variable rate of interest and the rate has changed

You’ve missed or underpaid mortgage payments in the past year

Fees or charges were added to your mortgage

We’ll always write to you to tell you if your monthly payment is changing.

Your mortgage balance could increase for a few reasons, such as:

You’ve missed or underpaid mortgage payments in the past year

You’ve chosen to add some fees to your mortgage instead of paying them separately. Interest will be charged on any fees added to your mortgage

Your December payment didn’t reach us until January, so will only appear on the following year’s statement

Some mortgages let you make overpayments that will reduce your mortgage balance. The amount you can overpay by each year without having to pay any fees or charges depends on the type of mortgage you have. The limit is usually 10% of the mortgage balance each year.

You can make overpayments by:

Bank transfer, for a faster payment

Name: this should match the name on your account with us.

Sort code: 40-64-38.

Account number: the first eight numbers of your existing 10-digit mortgage account number.

Card payment in branch, or over the phone via our secure automated payment line on 03300 081 604.

Cash or cheque in branch

If your mortgage product has daily interest, either of these options will reduce your balance on which interest is charged straight away.

If your mortgage product has annual interest, any overpayment must be for £1,000 or more to reduce your balance on which interest is charged straight away.

If you’re making an overpayment above your monthly mortgage repayment, there might be conditions or fees to pay, such as the Early Repayment Charge. Please remember to check the terms and conditions in your mortgage offer or contact us to check how much you can overpay without fees or charges.

Yes, just get in touch with us. You need to let us know at least three working days before your Direct Debit collection date if you'd like to change it. The new date you choose must be between the 1st and 25th of the month.

If your bank details change, you might have to set up a new Direct Debit for your mortgage payment. You can contact us to do this or send us a new Direct Debit instruction form. It can take up to 10 working days for the new Direct Debit to be set up.

You might be able to pay off your mortgage before the term end date. But you might have to pay an Early Repayment Charge and/or a Mortgage Exit Fee to do this. Check your mortgage offer for the fee you’ll be charged if you repay your mortgage early. If you can’t check your mortgage offer, call us on 03450 540 911. You can ask us to give you a redemption statement up to 30 days before the date you want to pay off your mortgage.

If the cost of living, or changes to your circumstances, are making it hard for you to pay your mortgage, we could help.

If you fall behind with payments, or are worried you might do, we’re here for you. Please get in touch on 08000 729 739. Our friendly, expert team can help you work out what your options are and the best steps to take. Just calling us about your mortgage won’t affect your credit rating. You can call Monday to Thursday 8am-7pm, Fridays 8am-5pm and Saturdays 9am-12.30pm (except bank holidays), or you can visit our mortgage payment difficulties page for support.

What can I do if I have an Interest Only mortgage and I'm concerned about repaying my outstanding loan?

If you don’t have a repayment strategy in place to repay the mortgage balance at the end of the term, you should contact us as soon as possible to discuss your options before your mortgage comes to an end.

If you already have a repayment strategy, make sure you regularly check it’s still appropriate.

As an existing mortgage member, you might be able to borrow more money against your property.

Borrowing more money depends on your property re-valuation, income, affordability and credit checks. Your overall mortgage balance will increase if you borrow more. Any additional borrowing will be secured against your property.

When you're buying a new home, you may be able to move your mortgage deal to your new home. This is also referred to as 'porting’ your mortgage. This means you’ll keep the existing mortgage deal. This option can be great if you have a low interest rate on your mortgage or want to avoid early repayment charges.

You may need to borrow more when you move house. Borrowing more money depends on your property valuation, income, affordability and credit checks. Any additional borrowing will be secured against your new home.

Depending on the type of mortgage you have, you might be able to rent your house out. You’ll need to get in touch with us so we can send you a Consent to Let pack, which contains all the information you’ll need to make the request. We’ll then talk to you to see if it’s an option in your circumstances.

There are several options available to you:

MoneyHelper. This is a free service that provides clear guidance to help you make informed choices.

Citizens Advice. They provide free, independent, confidential and impartial advice.

Independent mortgage brokers. Mortgage brokers help you explore your options and find a solution which works for you. They’ll give advice tailored to your individual circumstances; but keep in mind that some brokers may charge for their services.

Leeds Building Society isn't responsible for advice provided by third parties.

Your property could be repossessed if you don't keep up your mortgage repayments.